Operational weather risk is localized, individualized and is becoming more impactful than natural catastrophes. Climate resilience for business requires transcending the impact from catastrophic weather and also operating with everyday weather extremes.

If they have not done so already, companies should account for weather-related emergencies. Edward Sagal, “How To Prepare For The Next Weather-Related Crisis” – Forbes

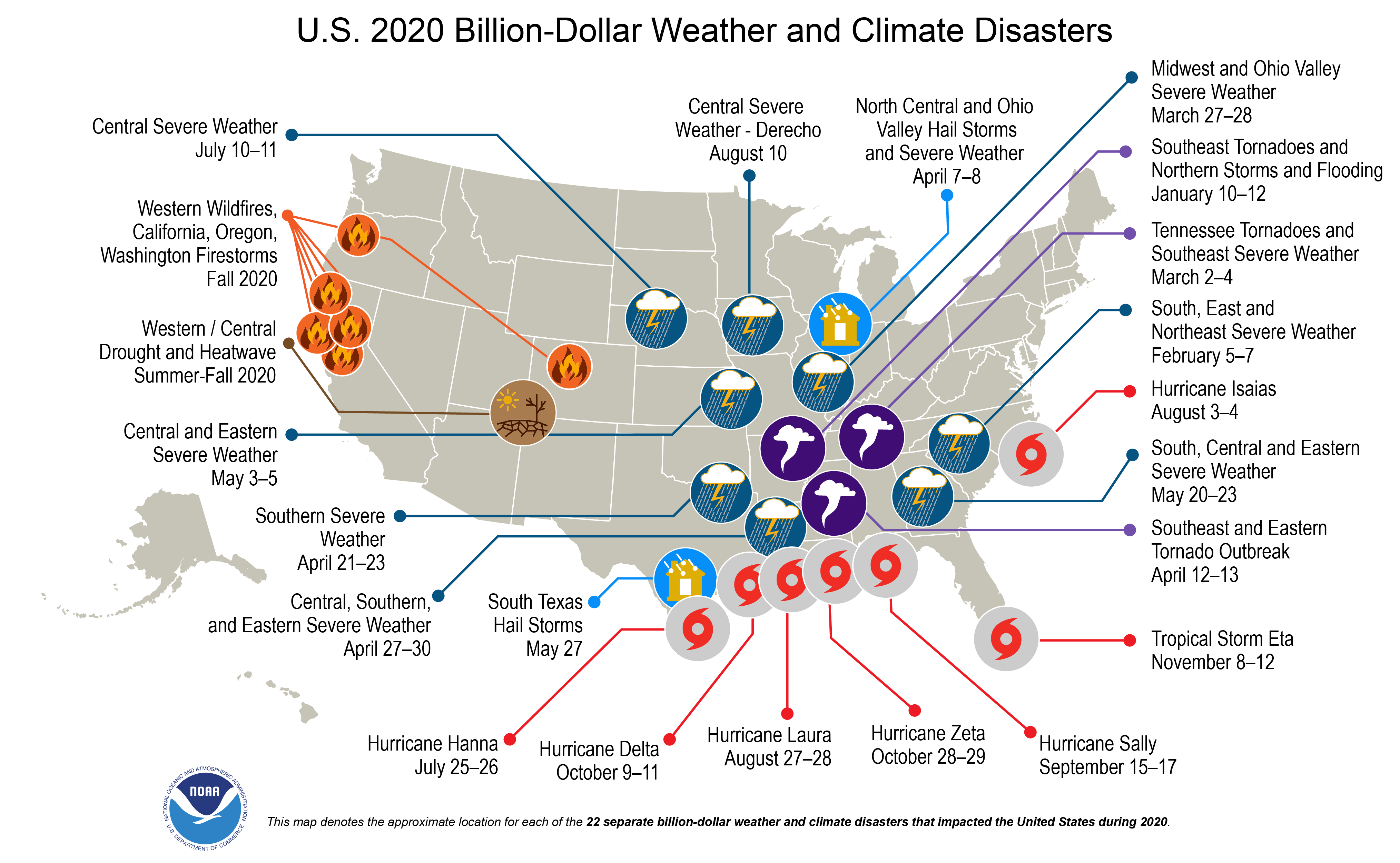

In 2020, there were 22 weather/climate disaster events with losses exceeding $1 billion to affect the United States. These events included 1 drought event, 13 severe storm events, 7 tropical cyclone events, and 1 wildfire event. Overall, these events resulted in the deaths of 262 people and had significant economic effects on the areas impacted. The 1980–2020 annual average is 7.0 events (CPI-adjusted); the annual average for the most recent 5 years (2016–2020) is 16.2 events (CPI-adjusted). NOAA Billion Dollar Weather Disasters

No matter the name, mid-February 2021 was cold in Texas

My friends in Austin called it the “freeze-pocalypse” and “Snowvid.” Capital Weather Gang called it an “Arctic plunge.” Many of us are also calling it Winter Storm Uri and the Polar Vortex.

Damage estimates from this deep freeze are well in excess of $10 billion which will make Texas’s freeze-pocalypse almost certain to be on NOAA’s top 10 list of 2021 billion-dollar weather disaster events.

Beginning on February 12th 2021 and continuing right through the following week, winter storms and freezing weather driven by a polar vortex event saw over 70% of the continental United States impacted with freezing temperatures, snow, and ice, with Texas seen as the state worst affected.

AIR Worldwide notes that there is likely to be a “significant number of expected claims,” while the average insurance claims severity value is likely to be around $15,000 for residential risks and $30,000 for commercial risks.

Add on the level of demand surge and AIR believes that insurance and reinsurance market losses “appear likely to exceed $10 billion.”

However, that figure could be much higher, AIR warns, noting that “there are several factors that could still potentially drive the loss well in excess of that figure.”

Among these are, “a higher than expected rate of claims among those risks affected by prolonged power outage, whether utility service interruption coverages pay out, larger than expected impacts from demand surge, government intervention, and whether claims from mold damage start to emerge as a significant source of loss.”

The industry seems to be converging on something north of $10 billion, but perhaps not as high as $20 billion, although demand surge and loss amplification could be the factor that results in a higher than anticipated industry impact. — Steve Evans, “Winter Storm Uri loss could be “well in excess” of $10bn: AIR” – Artemis

It was certainly cold but it wasn’t really THAT cold!!

Guess what, it gets cold in Texas in February!!

While the cold snap was in many ways historic, it wasn’t completely unprecedented based on climate data going back many decades; some past cold waves, such as one in 1899, surpassed it in severity. Andrew Freedman, John Muyskens and Jason Samenow, “Central states’ Arctic plunge: The historic cold snap and snow by the numbers” – Washington Post

1983 was cold in Texas.

1985 was cold in Texas.

1989 was cold in Texas.

2011 was cold in Texas.

2021 was cold in Texas.

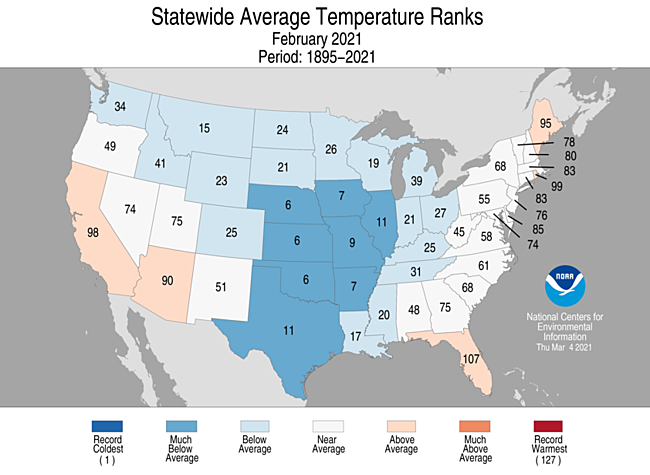

In fact, February of 2021 was the 11th coldest February in 127 years. 2021’s freeze-pocalypse didn’t even make the top 10!!

Andrew Siffert from bms explains how the 11th coldest February can drive so much economic loss in The Great Deep Freeze and Compounding Events

Extreme weather happens EVERY year

The last time Texas suffered freeze-pocalypse was in 2011. Anyone who has lived in Texas for more than a few years knows it gets cold. In fact, since 1979, there have been 33 days in Austin that dropped below 20 F. 9 of these very-cold days have occurred since the winter of 2009-2010.

The chart below from bms (courtesy Andrew Siffert – “The Great Deep Freeze and Compounding Events“) shows statistics for winter storms that caused insured loss for each winter between 1972-1973 and January of 2021 (not yet including Winter Storm Uri). Blue bars indicate the number of loss-driving winter storms and the secondary thinner bars indicate the total insured loss per year. Almost every winter since 1972 has featured at least one loss-causing storm!

What about Global Warming? Climate Change is certainly affecting global weather patterns but the result isn’t always intuitive. Winter storms will keep on coming.

Catastrophic Weather versus Extreme Weather

When I was on the team at Citadel around 2005, we seized an investment opportunity in catastrophic weather. Today, catastrophic risk is a mature and well-served industry with top notch investors and servicing companies. Most of you reading this are actually part of this market, even though you might not know it. If you have business insurance or homeowners insurance you are most likely part of the marketplace for catastrophic risk (aka cat-risk). Your insurance company most likely carries its own insurance (aka reinsurance). When a major catastrophe affects your home or your business, your insurance company pays you in an effort to help you recover your financial losses and rebuild. These catastrophes (such as earthquakes and major hurricanes) probably also affect your neighbor and your neighborhood and your town and the town next to yours. Your insurance company winds up paying a lot of homeowners and businesses in an effort to help large areas of society recover financial losses and rebuild. In this case, your insurance company may require insurance of its own to cover its own financial losses. That’s where the reinsurer steps in. The reinsurer pays your insurance company which then pays you (and lots of other people).

According to the Insurance Information Institute, catastrophic events are those that trigger losses exceeding $25-billion. The last catastrophic weather event (i.e. the last event to cause over $25-billion in in CPI-Adjusted Estimated Cost) was Hurricane Matthew in October of 2018.

Thankfully, catastrophic weather doesn’t happen every year. In fact, there have only been 15 weather events since 1980 that exceeded $25-billion. (Data courtesy NOAA “Billion-Dollar Weather and Climate Disasters: Events”

| Catastrophic Weather Event | Date | CPI-Adjusted Estimate Cost (in billions) |

| Hurricane Katrina | August 2005 | $170.0 |

| Hurricane Harvey | August 2017 | $131.3 |

| Hurricane Maria | September 2017 | $94.5 |

| Hurricane Sandy | October 2012 | $74.8 |

| Hurricane Irma | September 2017 | $52.5 |

| Hurricane Andrew | August 1992 | $50.8 |

| Drought / Heatwave | Summer 1988 | $45.0 |

| Flooding | Summer 1993 | $38.1 |

| Hurricane Ike | September 2018 | $36.9 |

| Drought / Heatwave | Summer 2012 | $34.5 |

| Drought / Heatwave | Summer-Fall 1980 | $33.5 |

| Hurricane Ivan | September 2004 | $28.9 |

| Hurricane Wilma | October 2005 | $25.8 |

| Hurricane Michael | October 2018 | $25.7 |

| Hurricane Rita | September 2005 | $25.2 |

Investors have been focusing on providing capital to cover these events since my time at Citadel, and there is a robust financial ecosystem providing financial resilience for weather catastrophes on a societal scale.

Non-catastrophic weather-extremes occur far more frequently. While there’s not an industry agreed standard what what categorizes non-catastrophic but extreme weather, let’s consider events that reach the $1-billion economic threshold. According to NOAA, these events occur in the United States almost every year.

The U.S. has sustained 285 weather and climate disasters since 1980 where overall damages/costs reached or exceeded $1 billion (including CPI adjustment to 2020). The total cost of these 285 events exceeds $1.875 trillion. NOAA: Billion-Dollar Weather and Climate Disasters: Time Series

Building Financial Resilience for Extreme Weather

For decades, the agriculture and energy industries have used risk markets to protect against the bottom-line impacts of weather. Today, more and more businesses are managing the impacts of a rapidly-changing climate and the lessons learned in energy and agriculture are starting to be applied on a larger scale.

We estimate there is approximately $70 billion of climate risk currently manageable in the United States alone, with over $7 Billion of this risk is borne by Municipalities, Universities, School Districts and Medical Campuses. Insurance companies and financial servicing companies outside of the well-established weather risk marketplaces in agriculture and energy are moving to address this market.

Companies ranging from mega-farming conglomerates to small-town corner bakeries can now mitigate the financial impact from weather extremes through parametric coverage.

For example, within the past 10 years, New York City has experienced its third-snowiest winter and its two all-time least snowy winters. Winter storms seem to be coming in “boom or bust” cycles from year-to-year.

Seasonal Snowfall Analysis courtesy Demex Solutions Center

This year-to-year variability drives dramatic cost fluctuations for property managers who must maintain passable sidewalks and parking lots. These companies spend very little in years with only little snow but they pay a lot more during snowy winters.

The reverse is true for the companies that service those sidewalks and parking lots. They make big money in snowy winters and can have extreme losses in a winter like 2019 when it rarely snows. Excess Snowfall Coverage allows both of these businesses to protect themselves against a bad year.

We estimate today’s global manageable costs and revenues linked to snowfall at $10B in the private sector and $80B in the public sector. The Demex team has covered over $50M in parametric snow risk.

Climate Resilience for Business Operation

Climate resilience requires planning for, operating within, and recovering from weather extremes.

Plan for future events: Assess risk and practice response

A detailed weather hazard risk assessment should be part of every organization’s business continuity and emergency preparedness reviews.

As business processes—and weather patterns—constantly evolve, a plan created five years ago is no longer applicable.

It’s valuable to partner with experts in meteorology and risk communication who are able to readily provide historical weather data and help translate that data into actionable information for your organization.

Emergency weather plans should be exercised (or tested) at least once annually, evaluated for effectiveness, and improved as needed.

While the activation of a plan during a real weather emergency will provide an organization with invaluable feedback, a discussion-based “tabletop exercise” is a safer and more predictable test of your plan. This type of exercise will enable you to identify health and safety gaps prior to the threat of a live event. A meteorologist can help your organization run this exercise, providing an accurate scenario based on their experience and expertise.

“Often, a professional meteorologist is asked to develop a mock weather scenario, provide briefings, and answer questions throughout the drill,”

Edward Sagal, “How To Prepare For The Next Weather-Related Crisis” – Forbes

Operate during extreme events: Use systems for alerting and understanding real-time risk

Keep abreast of weather alerts: Ensure that your team is well-informed about extreme weather that may be brewing days or weeks in advance. Optimize your information channels and work with experts to directly link your weather alerts to your business impact. Tailor your alerts so that they provide you enough lead-time to be proactive within the optimal range of forecast precision and accuracy. The weather forecast is likely to change day-after-day and it is important to be aware of changing information.

Deploy the the operational procedures that you’ve developed in the planning phase and practiced during the tabletop exercises.

It’s often helpful to engage applied meteorologists experienced in forecasting extreme and consequential weather events that affect operations like yours.

Leverage weather applications and media reports to gain deep real-time situational awareness.

Recover: Purchase Climate Coverage for Financial Operations

Speak with your trusted partners in insurance and financial services to discuss coverage options that will offset your financial losses when extreme weather occurs. Customized Parametric Insurance, Property and Casualty Insurance, Business Lines Insurance and/or Financial Derivatives are all commonly used methods for protecting against extreme weather related losses due to unexpected increase in costs or lost revenue. Relatively small preemptive premiums can provide significant financial recovery.

For example, recent years have brought extreme year-to-year fluctuations in snowfall in Toronto, Canada.

Seasonal Snowfall Analysis courtesy Demex Solutions Center

Toronto’s best and worst winters have both occurred since 2000. Canadian airport parking operator, Park’N Fly is particularly sensitive to snowfall with highly volatile snow removal expenses year-to-year at the seven airports they operate parking facilities for. Their snow removal costs can be more than twice as high during a “snow-pocalypse” winter versus a year with a “snow drought.” Using weather, climate and local geographic data, our tech here at Demex assessed the likelihood that snow removal costs would exceed Park’N Fly’s budget in any given year. We partnered with Munich Re and Nephila Climate to build coverage that caps Park’N Fly’s spend on plowing and salting. This coverage provides predictability of snow removal costs year-to-year, capping total expenses.

Carlo Marrello, Chief Executive Officer, Park’N Fly said it best, “The Demex Group allows Park’N Fly to mitigate its risk associated with the variability and unpredictability of snow removal costs. The Demex solution has brought cost certainty with its innovative cost protection solution. This solution has positively impacted snow removal expenses while delivering fixed costs for budgets and better fiscal management.”

Snow isn’t the only weather extreme for climate coverage. We’ve worked with insurance brokers who cover country clubs. One such club in Missouri has on-site reservoirs for irrigation. In a very dry year, such as 2018, they don’t have enough of their own water. They needed to buy water from the local municipality. This led to hundreds of thousands of dollars in unplanned expenses. Businesses like this can spend a small fraction of that amount in a preemptive premium and receive full coverage when they are forced to buy water in that dry year.

On the flip side of that coin, we worked with a broker who covers a golf course in Kansas where over 4 inches of rain fell on a single day, causing significant damage to the landscaping and unplanned expenses in the six figures. It’s the same concept; they can pay a fraction of that in premium and the business gets coverage to offset these unplanned costs.

Our customers interactively set their coverage window, deductible and limit. Once they’ve found a plan they like, they can immediately apply for coverage.

We also work with insurance carriers to embed climate resiliency solutions directly into their existing products, such as homeowners or business lines. These products are made accessible to insurers and their customers via a Demex API. We offer customers real-time, localized pricing for every ZIP code in the U.S. as well as millions of locations around the world.

Our early adopters include commercial real estate owners and their servicing companies. We’ve also crafted coverage for construction companies that face penalties when weather causes project delays. Travel and leisure companies – especially beach/ski resorts and golf courses – are also early targets for climate resilience along with schools, hospitals, municipalities, and retailers.

Learn more about Demex and how we work together with insurance and financial service professionals to build climate resilience for businesses around the globe.